Introduction

Autonomous vehicles bring fear. As their job prospects are being threatened, taxi and truck drivers are feeling anxious to brace themselves for the disruption. For car and truck insurers, the argument usually goes like this: automation will make vehicles so much safer, to the point where no accident will happen hence no insurance is required. This concern is ill-founded, and this article serves as an illustration. More broadly, this article endeavours to present insurance-related challenges brought by autonomous vehicles to insurers and vehicle manufacturers, and attempts to find solutions for these challenges.

Challenges will be discussed in accordance to the organisations to which they apply, immediately followed by solutions.

Background and Context

It is imperative to note that as of the writing of this article, we are still at the early stage of the development of autonomous vehicles, with no fully-autonomous vehicles commercially available to the ordinary consumers. Right now we have autonomous buses running on confined sites such as university campus or sports park, but this application is hardly complex enough to contribute meaningfully to the issues at hand. Currently the most commercially successful partially-autonomous cars are developed by Tesla, but even its Autopilot system requires human intervention under many circumstances and establishing liability at an accident is still a tricky business for the courts.

Some authors like to decompose the development of autonomous vehicles into stages or phases as an attempt to facilitate understanding. To avoid over-complication, there are only three meaningful stages for insurance purposes: minimally-autonomous (cars in 2017), partially-autonomous (if everyone has a Tesla in 2017), and fully-autonomous. The first phase, minimally-autonomous, will not be a topic of discussion in this article since insurance for this type of vehicle has existed for nearly 100 years and has remained unchanged for the most part. The second and third phases are the main focuses of this article. Each phase has its unique challenges, but we will see shared challenges as well.

Let us now define the phases. The year 2017 is in the minimally-autonomous phase. Here most cars may have cruise control (automatic control of speed) and automatic braking, but this is as far as automation goes. Fully-autonomous is self-explanatory. This is when most people use cars that do not require a driver at all, with the car driving itself under all circumstances at all times. The definition of partially-autonomous is not as definitive, because this includes everything between minimally- and fully-autonomous. The best example is if everyone was driving a Tesla in 2017. These cars can autonomously drive themselves under certain circumstances (such as highways), but they still require a driver’s active attention to the surroundings and expect drivers to take back control frequently.

Challenges Faced by Insurers and Solutions

The most significant concern for car and truck insurers is that autonomous vehicles will hurt their revenue. The extreme version of this argument is that fully-autonomous vehicles will become so safe that society does not need vehicle insurance anymore. This is unlikely to occur because despite humanity’s relentless effort, no engineering product is perfect and flawless. Even fully-autonomous vehicles will have issues that cause accidents, hence presenting risks that insurance can mitigate. There will however, be a major change. In the world of fully-autonomous vehicles, liability for loss will shift from the consumer to the manufacturer of the vehicle. This is because we no longer have such thing as a driver, and all driving responsibilities fall onto the vehicle’s software and hardware. When one is not responsible and is not in control of the vehicle’s operation, we cannot hold one accountable for losses. In other words, car insurance will transform into product liability insurance, and no individual consumer needs to take out car insurance.

A more moderate version of the above concern is that, automation will make vehicles safer, hence decreasing insurance premium. This is reasonable, but we must not disregard the fact that claim cost for insurers will decrease at the same time. As we are still very far from mass adoption of fully-autonomous vehicles, it is very difficult to predict the proportionate decrease of claim cost. If claim cost decreases at a higher rate than that of the decrease in premium, this may not be the end of the world. However, due to the unpredictability, insurers need to focus on things other than price in order to gain competitive advantage. In-house knowledge of autonomous systems is a must, and insurers need to start developing this capability now. Underwriters need to understand how autonomous systems respond to different road and weather conditions, such as construction zones, road closures, and blizzard. They also need to have an appreciation for the diagnostics that manufacturers have to maintain the systems and how quickly updates are pushed out and executed. Moreover, data is key. When vehicles become more machine-driven, insurers have fewer excuses to not utilise data to the fullest extent. Most insurers already have some data analysis capability for actuary purposes, but they need to get prepared for the extra amount of data collected by ever more sensors on the vehicles.

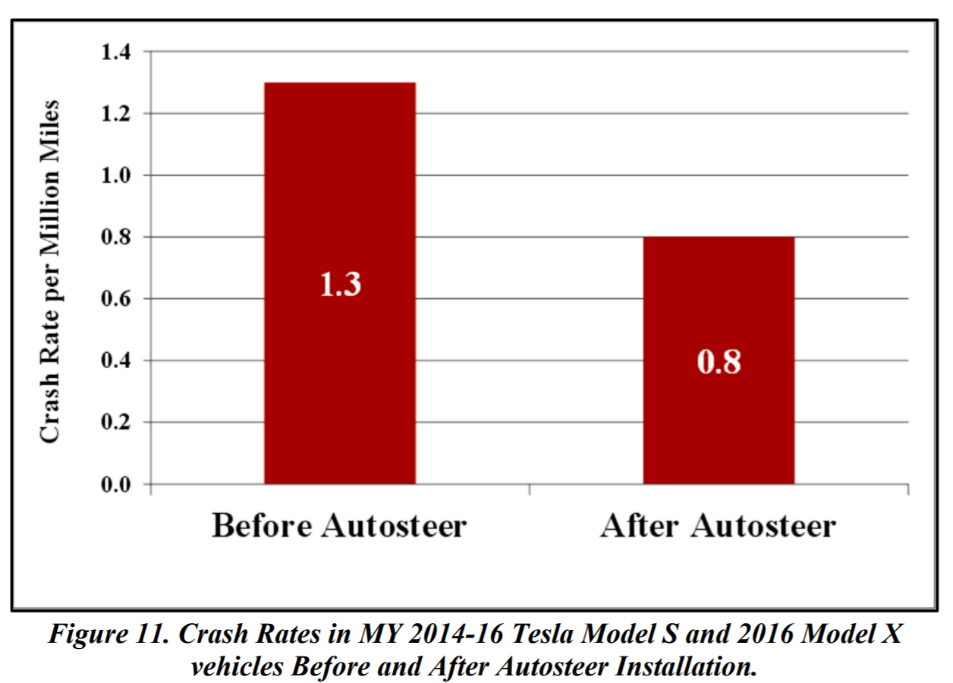

If we turn our eyes to another problem, we see a conundrum. On one hand, we have evidence to show that automation does make vehicles safer. Even with Tesla’s partially-autonomous Autopilot system, we can see the clear result below.1

The crash rate per million miles has decreased significantly from 1.3 to 0.8 after Autosteer was installed. That is nearly a 40% reduction in crash rate. On the other hand, we can imagine that because all autonomous vehicles from one manufacturer will use the same hardware and software, if there is one fault in the vehicle, it will be the same fault for all vehicles and this has the potential to cause an enormous amount of vehicles to malfunction simultaneously and result in a large claim (just imagine a hacker gains access to millions of vehicles at the same time). What this means is, the nature of car insurance will be transformed from high frequency & low severity to low frequency & high severity. This presents a huge risk profile for insurers. The solution is surprisingly elegant and powerful because it solves two problems simultaneously. So let us take a look at the next problem first, then the solution.

It was mentioned above that the insurance burden will shift from consumers to car manufacturers, but basic economics tells us this is a very deep problem. The number of future manufacturers requiring product liability insurance will be significantly smaller than the number of today’s drivers requiring car insurance. So when fully-autonomous vehicles become commonplace, the number of clients for insurance will be significantly lower than that of today’s, yet the number of insurance suppliers will remain the same (at least initially). Each insurance client will require insurance for many more vehicles, but the number of clients will decrease (basically to the total number of vehicle manufacturers). This gives manufacturers tremendous market power. They will have more leverage in negotiating premium and coverage, and this will hurt insurers’ bottom line. What is more concerning, is that because the number of clients is so small, the market size is so small, that it does not have room for many insurers. Some insurers may see a forced exit out of the market.

In order to avoid manufacturers having too much market power and to avoid having too much risk due to vehicles sharing the same build, insurers need the help of regulators and policy makers. We may be able to impose manufacturers to insure their vehicles with multiple insurers. For instance, 10% of a car model insured by insurer A, 10% of the same model insured by insurer B and so on, and the same rule applies to all models. Manufacturers can choose which insurers they want to work with, but within each model of car, they have to use different insurers, and all insurers insure the same proportion of the model. Here are the merits of this solution. The purpose of insurance is that we take the premium from safe drivers, and use this money to pay for accidents caused by unsafe drivers, then hope we have money left. This business model will not work if a manufacturer chooses one single insurer to insure all of their vehicles and the insurer cannot get more clients because of the small market size. Manufacturers will be inclined to do exactly this in a world of fully-autonomous vehicles because this saves premium, is easier to manage, and grants them more negotiating leverage. Insurers will try to fight this but will struggle to find clients due to the limited number of clients available. This is where the regulation comes in. The market power of manufacturers is reduced by requiring them to use multiple insurers. Competition amongst insurers is sustained by allowing manufacturers to freely choose insurers. The risk borne by insurers is reduced by requiring each car model be insured by different insurers, sharing the risk evenly.

Things can get extremely tricky when we are in the partially-autonomous phase. Specifically, the determination of liability in the event of a car crash. Since partially-autonomous cars can drive themselves in some situations but require human control in others, the responsibility of an accident can take long to be established, as we see with Tesla cars today. Ultimately, liability shall be determined by the courts on a case-by-case basis, but we can still try to minimise the resources and time needed by the courts. Just like air planes, all autonomous vehicles, regardless of level of automation, should have a ‘black box’ to record all data gathered by sensors onboard, ideally including conversations taking place in the car. Due to the sensitivity of privacy, regulators are unlikely to allow in-car conversation to be recorded, but they can at least obligate that all vehicles must be installed with a black box that can sustain extensive impact and pressure. This black box will prove instrumental in the decision-making process of courts and jury, depicting a clear picture of what took place at the accident.

Challenges Faced by Car Manufacturers and Solutions

We have already seen that, as vehicles become more autonomous, liability will shift from consumers to vehicle manufacturers. This in turn means the burden of taking out insurance now lies with manufacturers. But it is not rational for manufacturers to see this as a burden, since insurance is meant to protect them. In addition, manufacturers have much to gain in this automation revolution, and insurance premium is a price worth paying.

When the vehicle hardware or software is deemed responsible for an accident, it is conceivable that the fault is not in the vehicle manufacturer, but its ‘downstream’ suppliers, vendors, or subcontractors (let’s call them partners). In the interest of protecting themselves, it is therefore essential for manufacturers to put in an insurance clause in their contracts with any partners. This insurance clause shall stipulate that the partner is obliged to obtain insurance and if the partner is found to be legally liable, subrogation will occur. This not only protects the manufacturer, but also assists the manufacturer’s insurer in seeking recovery from the partner.

Cyber liability exposures arise when vehicles are ever more reliant on computer systems and telecommunication. Hacking and digital virus are some of the biggest challenges faced by organisations and individuals today, and this problem will only become more acute when what is vulnerable is as dangerous as cars. The possibility of hacking into a moving car was demonstrated in July 2015, with two American hackers remotely gaining control to, among other things, the engine of a driving Jeep while a journalist was driving it on a highway.2 The engine stopped in the middle of the highway while the car was moving, but fortunately no one was hurt because the journalist asked the hackers to perform the attack. Now, imagine the hacker was in fact malicious and you were sitting in the car. To prevent this, manufacturers need to ensure software on cars are always up-to-date. This requires manufacturers to constantly test for bugs, build an update as soon as a bug is discovered, and force update installation on cars as soon as update is released. Manufacturers also need to prevent the consumers from tampering with the software. The software should not allow any alteration, and if it detects any attempt to alter, an alarm is raised with the manufacturer and the car should cease to operate when it is safe to do so.

Perhaps the most delicate business for manufacturers in the world of partially-autonomous vehicles, is to effectively communicate to consumers that vehicles do require human intervention, and to ensure consumers do actively intervene when necessary. Many consumers of autonomous vehicles currently give their vehicles more faith than the vehicles deserve, and this can cause accidents and unnecessary disputes. What manufacturers need to do is to thoroughly educate consumers before they purchase the vehicle, and upon purchase, have the consumer sign a legal declaration stating they have understood the safety requirements and will comply fully. What can also be included in the declaration is a promise not to alter the vehicle software.

Final Words

It is likely that automation will reduce individual car ownership drastically and corporates will own large fleets of autonomous vehicles. All the conclusions detailed in this article apply to both individual car ownership and corporate ownership.

Autonomous vehicles will bring immense benefits to human society. We will get safer roads, shorter commute time, better use of commute time, and reduction in carbon emission. This will, however, take decades to accomplish, but everyone has a role to play in accelerating this revolution. Insurers, manufacturers, and regulators all need to collaborate to enable the future. There will be obstacles to overcome, but our collective effort shall bring us one step closer to success.

Reference

- National Highway Traffic Safety Administration. (2017). ODI Resume. Retrieved from https://static.nhtsa.gov/odi/inv/2016/INCLA-PE16007-7876.PDF

- Greenberg, A. (2015). Hackers Remotely Kill a Jeep On The Highway – With Me In It. Retrieved from https://www.wired.com/2015/07/hackers-remotely-kill-jeep-highway/